Investor note

Sell, Do Not Transform. The New Private Equity Answer When the C-Suite Cannot Change Fast Enough

The consensus inside private equity is that the AI transition is an operational value-creation problem. Buy the underperforming software asset, fund the transformation, hold through the curve, exit richer. The logic is reasonable on its face, and it fits the moment. With multiple expansion gone, operational improvement is now the dominant value lever: about a third of deal teams rank it as the single most important driver of the equity story, almost double the next lever, and 78 percent expect it to grow further over the year ahead [Simon-Kucher, 2025]. So AI-native conversion gets filed as the next operational programme. For a widening class of software assets, that filing is wrong.

The mispricing is in the denominator most models ignore: the C-suite’s rate of change. AI-native conversion is not a systems upgrade. It reorders where decisions sit and who holds them, which is why it is more a political reset than a technical one. If the incumbent C-suite cannot rewire fast enough, the programme does not run slowly. It does not run. And the bill is not theoretical. Full-scale transformations carry an observable 18-month track record before returns show up, and roughly 70 percent of them fail to meet their objectives [McKinsey; BCG]. Underwriting AI transformation at SaaS-era confidence misprices the most binding input in the model, and it is the one input a data room does not show you.

This is where the decision flips from transform to dispose. If the honest conclusion, after scoping the full transformation, is that the cost and disruption for the current owner exceed the gain, especially given how fast that leadership could realistically change, then the rational move is to sell the asset to an owner who has already made that shift. That owner would keep the parts that work. The current owner would avoid funding up to eighteen months of surgery to reach the same place at a worse price. You did read it right: up to eighteen months is what it could take, on average, to fully transform and change the trajectory of even a small ($10-$20M ARR) software asset.

The question is no longer how to fund the change, but whether this C-suite can change faster than the market reprices the asset.

The market now rewards exactly that sorting. Public SaaS multiples have compressed from 6.2x EV/revenue at year-end 2024 to 4.9x at year-end 2025 to roughly 3.3x by the end of March 2026, with around a trillion dollars of SaaS market capitalisation erased in the first quarter of 2026 alone [Aventis Advisors; Software Equity Group]. At the same time, assets with genuine AI capability command 30 to 50 percent premiums over comparable non-AI software [FinancialContent, 2026]. The market is bifurcating into AI-enhanced and AI-threatened, a sorting covered in detail in Software multiples in the agentic era and The SaaSpocalypse mispricing. For a threatened asset, transformation is a bet that the C-suite can move the company across that line before the discount becomes permanent. The disposal answer is the recognition that, for some teams, the bet is not worth funding.

State the downside case honestly, because the error runs in both directions. Some assets are worth transforming, the ones with proprietary data, real distribution, or a workflow position that survives agentic substitution. There, funding the change is rational, because the destination is defensible and the buyer would capture the upside you walked away from. Sell one of those too early and you have handed the moat to someone else at a discount. Transform one whose C-suite cannot change and you burn eighteen months while the discount widens. The judgement is not transform-versus-sell as a doctrine. It is whether this specific C-suite can change faster than this specific market repriced the asset.

The macro removes the luxury of waiting to find out. Holding periods are at record highs, a median of about 5.8 years, and the backlog of buyout-backed companies held longer than four years has reached roughly 16,000 globally, around 52 percent of total inventory [S&P Global; McKinsey, 2026]. Owners sitting on aged software assets cannot assume a patient transformation window is available. The exit clock and the AI clock now point in the same direction, which makes the transform-or-dispose question urgent rather than philosophical.

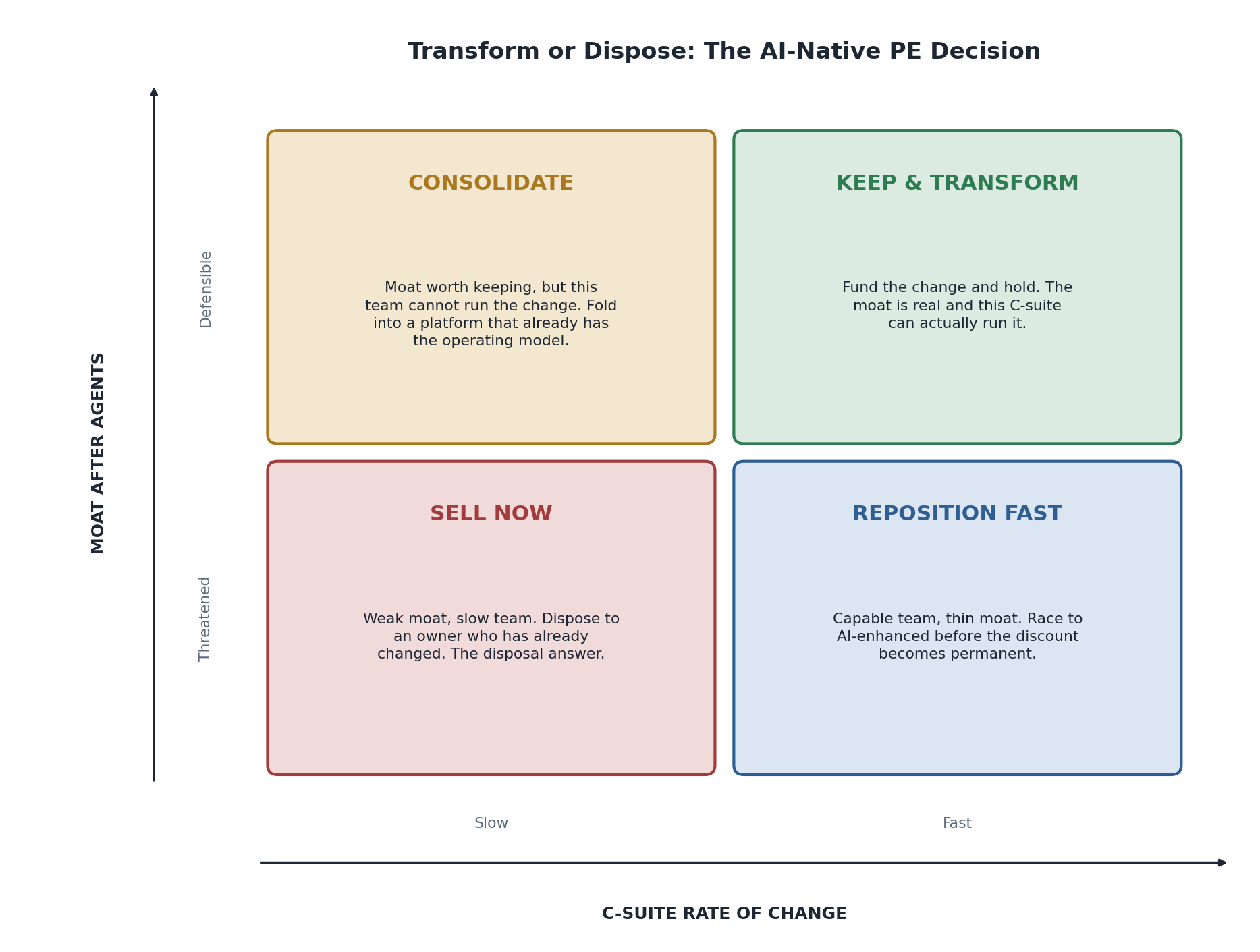

Two axes decide the question. The vertical axis is what survives the agents: the asset’s moat after substitution. The horizontal axis is the C-suite’s demonstrated rate of change. Those two axes give four moves, not two. Keep and transform when the moat is real and the team can run the change. Sell now when neither holds. Between them sit two middle paths that most underwriting collapses too quickly. When the moat is real but the team cannot run the change, the move is usually to consolidate: fold the asset into a platform that has already built the operating model, preserving the moat and importing the capability the incumbent C-suite lacks. When the team is capable but the moat is thin, the move is to reposition fast, racing the asset to AI-enhanced before the discount sets.

The trap is in the two upper boxes, and it is the same trap in both. Investors systematically overestimate two things: their ability to transform an asset, and their ability to change a C-suite on the clock the market is running. Transformation fails roughly seventy percent of the time even when leadership cooperates [McKinsey; BCG], and replacing a C-suite is slower and noisier than any deal model assumes. So assets that belong in sell-now get parked in keep-and-transform, and assets that belong in consolidate get held as if the incumbent team will be swapped cleanly and on schedule. This is the single thing an LP should test in a value-creation plan: not the ambition of the transformation, but the evidence that this manager can change this team faster than this market is moving. Absent that evidence, the honest default is to bias every asset one box down and one box left of where the deal team has placed it.

Locating an asset takes more than one question per axis. For the moat, ask three.

- Does the product own proprietary data or a system of record that a competitor cannot reconstruct?

- Does it hold the workflow and the distribution, or is it only a feature that an agent can replicate?

- And what share of current revenue sits in seats or tasks an agent removes within twenty-four months? For the C-suite, ask three more.

- Which executives have personally rebuilt their own work with AI, rather than sponsored a programme for the org below them?

- How fast has this exact team executed a comparable structural change before, with dates, not intentions?

- And is the board both willing and able to replace the non-adapters inside two quarters, not two years. For the synthesis, ask the last three.

- What is the fully loaded eighteen-month transformation cost and disruption against the discount to a clean-sale price today?

- Who is the natural consolidator if the moat is worth preserving but the team is not?

- And at what point does continued holding convert a transformation thesis into a sunk-cost one?

Watch the C-suite’s demonstrated rate of change, not the transformation plan’s ambition.

The plan is the easy part. The team is the asset, or the liability, and the most expensive error in this cycle will be transforming the assets that should have been sold.

Sources

- Simon-Kucher, “PE Value Creation Study 2025.” https://www.simon-kucher.com/en/insights/private-equity-study-2025 (accessed 2026-06-05). Operational improvement ranked the top value lever by roughly one third of deal teams; 78 percent expect it to grow.

- Aventis Advisors, “SaaS Valuation Multiples: 2015-2026.” https://aventis-advisors.com/saas-valuation-multiples/ (accessed 2026-06-05). EV/revenue multiple compression across 2024 to 2026.

- Software Equity Group, “2026 Annual SaaS Report.” https://softwareequity.com/research/annual-saas-report (accessed 2026-06-05). Public SaaS multiple trend and deal selectivity.

- FinancialContent, “The Great SaaS Reset: B2B Software Equities Plunge 25% as AI Disruption Rewrites the Playbook,” 26 March 2026. https://www.financialcontent.com/article/marketminute-2026-3-26-the-great-saas-reset-b2b-software-equities-plunge-25-as-ai-disruption-rewrites-the-playbook (accessed 2026-06-05). Roughly $1T SaaS market cap erased Q1 2026; 30 to 50 percent premium for genuine AI capability; AI-enhanced versus AI-threatened bifurcation.

- McKinsey & Company, “Common pitfalls in transformations.” https://www.mckinsey.com/capabilities/transformation/our-insights/common-pitfalls-in-transformations-a-conversation-with-jon-garcia (accessed 2026-06-05). Roughly 70 percent of large-scale transformations fail to meet objectives; 18-month track record window.

- S&P Global Market Intelligence, “Private equity buyouts record longer holding periods in 2025,” December 2025. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/12/private-equity-buyouts-record-longer-holding-periods-in-2025-96348743 (accessed 2026-06-05). Record holding periods.

- McKinsey & Company, “Global Private Markets Report 2026,” cited via S&P Global and McKinsey private-capital insights. https://www.mckinsey.com/industries/private-capital/our-insights/beating-the-odds-how-private-equity-firms-can-improve-exit-prospects (accessed 2026-06-05). Exit backlog of roughly 16,000 companies, about 52 percent of buyout inventory.