Essay

The SaaSpocalypse Mispricing. Why the Rebound Will Be Bifurcated.

A short public-market presentation has been circulating across software investor desks through May 2026, arguing that the post-SaaSpocalypse selloff overshot and that the asset class is set up for a coordinated recovery (May 2026 SaaS Rebound deck). The deck treats the index as a single recovery trade. The structure says the opposite. The first growth curve in B2B software, the on-premise to SaaS migration, monetised a stable workflow at the seat. The second growth curve, SaaS to AI-native, breaks the seat as a unit and breaks the gross margin floor as a structural constant. The post-SaaSpocalypse rebound is not a return to the old curve. It is the public market starting to sort the old curve from the new one. Reading it as a flat recovery costs the operator and the investor two quarters they cannot afford.

The old growth logic, and why a flat rebound bid looks credible

The first growth curve rewarded a narrow set of behaviours. Seat-based pricing aligned customer value to user count. Multi-tenant architecture turned every extra customer into operating leverage above an 80 per cent gross margin floor. Services revenue masked product gaps without breaking the model. Renewal mechanics did the heavy lifting, and Rule of 40 underwrote the multiple. The capital industry, public and private, built its valuation work, board agendas, and incentive plans on that profile. A rebound bid that reads “buy back the index” is the entirely rational habit of a market that has spent fifteen years rewarding one shape.

That shape stopped paying after the February 2026 selloff. Triggered by OpenAI’s Operator release on 29 January and the launch of Claude Cowork on 24 February, the iShares software ETF IGV fell more than 21 per cent year-to-date through late March, and more than USD 2 trillion in software market capitalisation was erased (FinancialContent SaaSpocalypse summary, March 2026; Humai, AI agent context, 2026). Claude Cowork alone wiped USD 285 billion in 48 hours (Humai, 2026). What the market repriced was a specific operating model, not the category. The May rebound deck implicitly bets that an index repriced is an index recovered. The structure says only part of the index gets back up.

The hidden break, and why the rebound bifurcates

The break is on the cost line, not the demand line. AI-native delivery introduces per-call inference cost as a variable inside cost-of-revenue. ICONIQ’s January 2026 State of AI snapshot found inference averaging 23 per cent of total revenue at scaling-stage AI B2B companies, with AI product gross margin sitting at 52 per cent, up from 41 per cent in 2024 and 45 per cent in 2025, against the 80 per cent SaaS norm (SaaSMag, AI COGS analysis, 2026; The SaaS Academy, AI COGS guide, 2026). Public SaaS companies have started disclosing inference-related cost ratios between 4 and 9 per cent of revenue inside MD&A; the new operating range named in Q4 2025 and Q1 2026 prints is 60 to 70 per cent, not 80, and the compression is being labelled structural, not transient (SaaSMag, 2026; TechTimes on token tax, June 2026).

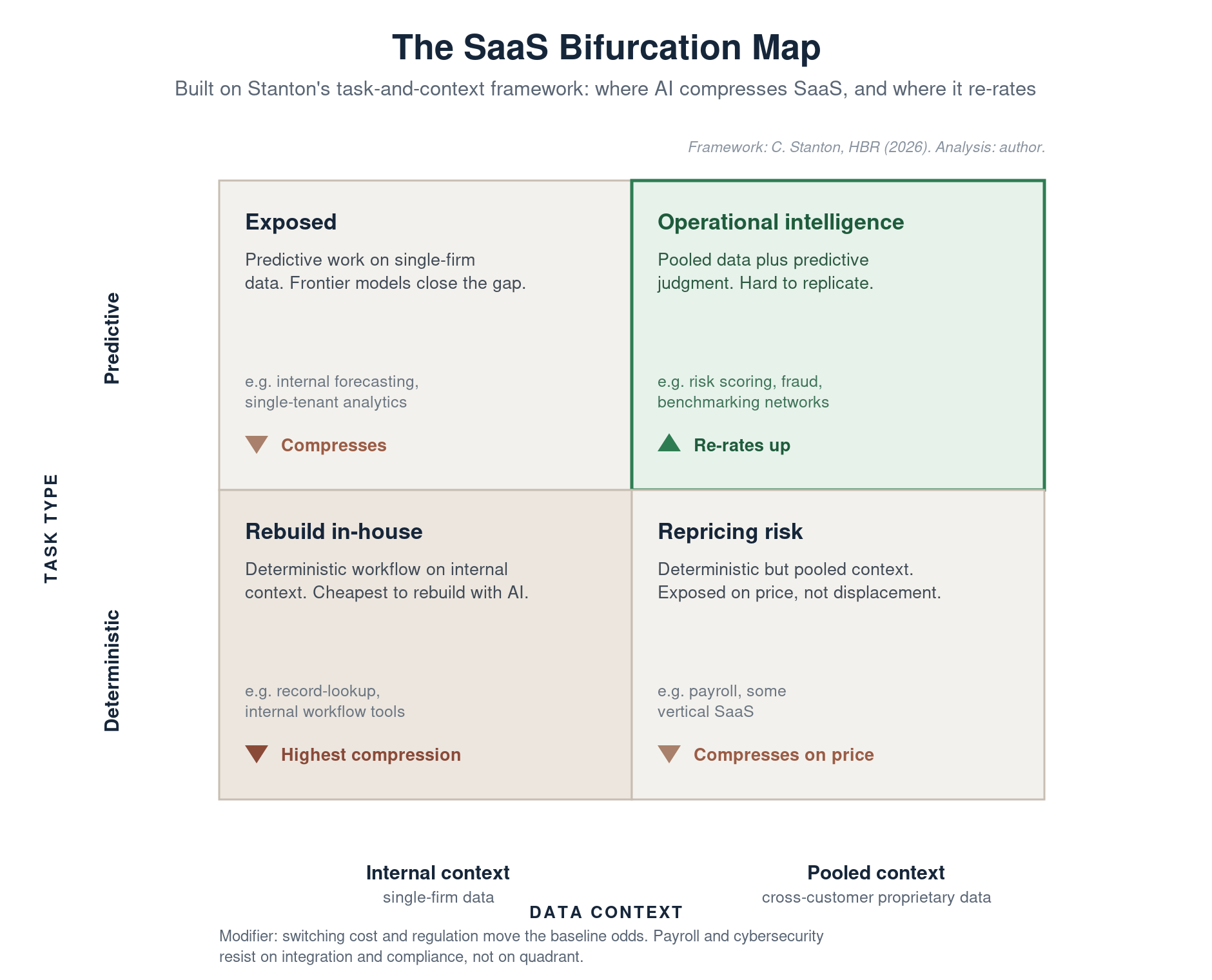

Christopher Stanton, Marvin Bower Associate Professor at Harvard Business School, gives the diagnostic that resolves the bifurcation. His May 2026 HBR piece argues that generative tools lower the cost of building deterministic, internally-focused software, exposing workflow and record-lookup SaaS to consolidation or in-house rebuild; SaaS that combines pooled proprietary data with predictive tasks is structurally different, embedding judgment and long-tail edge-case capture that single-firm data and frontier models cannot easily replicate (HBR, Stanton, 27 May 2026). The lens is a 2x2: deterministic versus predictive task on one axis, internal versus pooled context on the other. Three quadrants face compression. The fourth, predictive plus pooled, re-rates upward.

Figure 1. The SaaS Bifurcation Map. The deterministic-and-internal quadrant faces the highest compression, the cheapest to rebuild in-house. Deterministic-and-pooled compresses on price rather than displacement. Predictive-and-internal is exposed as frontier models close the gap. Only predictive-and-pooled, the operational-intelligence quadrant, re-rates upward. Switching cost and regulation move the baseline odds. Quadrant taxonomy from Christopher Stanton, “AI’s Impact on SaaS Will Be Uneven,” HBR, 27 May 2026; compression and re-rating overlay, quadrant verdicts, and examples by the author.

This is where the Second Growth Curve foundation needs amendment, not contradiction. The foundation argued that the SaaS-to-AI-native shift is a business-model reset and that the cost line is where the break happens (Gupta, The Second Growth Curve, May 2026). Stanton agrees on the structural call and adds a board-usable diagnostic that the foundation does not name. The borrowable lens is operational intelligence as the survival category, anchored in pooled judgment, not in feature shipping or per-seat leverage.

What this changes in the operating model and the underwriting

For the operator, the diagnostic precedes the pricing decision. The foundation sequencing was pricing first, then go-to-market, then product boundaries. The amendment is to insert a quadrant call ahead of all three. A B2B software CEO who cannot name which quadrant the company sits in, and which line of the customer’s pooled data the product is allowed to touch, will reprice into the wrong margin floor. The first board move is a portfolio map of the product line against the Stanton matrix, signed by the CPO and the CFO. The second is a renegotiation of the pricing model only after the quadrant is set.

For the capital allocator, the rebound deck is a list-price quote on an unsorted basket. The post-selloff redeployment that worked in past cycles, buy back the index and hold, prints a flat return at best in a sorting market. The capital response that fits the structure is the take-private. Thoma Bravo and Vista, the two software-focused private equity platforms with USD 120 billion deployed since 2019, used the H2 2025 and Q1 2026 window to lift Dayforce at USD 12.3 billion, Olo at USD 2 billion, and Verint at USD 2 billion off the public tape, with Thoma Bravo subsequently closing PROS Holdings (Bloomberg, Thoma Bravo on AI threat, 11 February 2026; Thoma Bravo press release, PROS Holdings). Orlando Bravo’s public position is that specialised software dominating discrete processes, payroll and cybersecurity in his examples, remains resilient. That is a quadrant call dressed as a sector call.

The implication for the public-market rebound is that the bid is correct on a minority of the index and wrong on the majority. The survivors carry pooled-data moats and predictive economics. The compressed names carry deterministic workflow and internal context. A blanket recovery trade pays the average. A quadrant-aware redeployment pays the right side of the split.

The counterargument, and where the foundation could be wrong

The strongest objection to a bifurcated read is that switching cost, distribution, and regulation save deterministic vendors that the framework would otherwise compress. Stanton allows this explicitly. A payroll system that owns the bank-feed integration and the regulatory filing posture is hard to rip out even when an AI build looks technically credible. A cybersecurity vendor with embedded sensors and incident-response institutional memory carries a moat the matrix does not draw. The amendment is therefore qualified: quadrant placement sets the baseline odds; switching cost and regulation move them.

The second objection is timing. The May 2026 rebound could be liquidity returning to a beaten-down asset class rather than structural sorting. Two earnings cycles will tell. If Q3 and Q4 print convergence across the matrix, with deterministic-quadrant vendors holding margin and predictive vendors compressing, the foundation thesis needs material revision. If they print divergence, with the survivors re-rating and the compressed names breaking lower, the bifurcation call holds. The author would update materially on convergence, especially if inference-cost curves bend the 60 to 70 gross margin floor back toward 80 (NVIDIA Perspectives on inference economics, 2026).

The third objection is sequencing. The foundation argued pricing first. If Stanton is right, the diagnostic step precedes pricing. The amendment treats the foundation as correct in direction and incomplete in sequencing. Pricing remains the first lever a board can actually pull, but it is pulled after the quadrant is named, not before.

The board agenda

Three moves for the CEO or CFO holding a SaaS stack.

First, rebuild deterministic workflow tools internally with AI coding where the vendor sits in the compressible quadrant and switching cost is low. The Stanton call is consolidation or in-house build. Atlassian’s experience inside the selloff, where Claude Code is reported to be substituting internal coordination work that previously sat in Jira and Confluence, is the pattern at scale (FinancialContent, March 2026).

Second, renegotiate vendors trapped in the compressible quadrant where switching is hard. A vendor with deterministic context but high regulatory or integration moat is exposed to repricing, not displacement. The negotiation is on price and on AI-feature inclusion at the existing seat envelope, not on the licence.

Third, double down on pooled-data predictive vendors where the switching cost is judgment, not data migration. Operational intelligence vendors will absorb work the operator’s team cannot easily replicate. The capital question is whether to buy more of them and whether to centralise the relationship at the CIO or the line owner.

The board question that should replace the SaaS-era one is direct. Which quadrant is each material vendor in, and which line of the profit-and-loss does the quadrant move first.

What would change my mind

Two quarters of earnings that print convergence rather than divergence across the matrix. A meaningful bend in the inference-cost curve that lifts the gross margin floor back toward the SaaS norm. A pooled-data vendor losing margin to an in-house substitute that closes the judgment gap with frontier models alone. Any one of these moves the call from bifurcation to repricing. The matrix is a lens, not a law.

Sources

- Christopher Stanton. AI’s Impact on SaaS Will Be Uneven. Here’s What Leaders Need to Know. Harvard Business Review, 27 May 2026. https://hbr.org/2026/05/ais-impact-on-saas-will-be-uneven-heres-what-leaders-need-to-know

- Vijayanta Gupta. The Second Growth Curve. May 2026. https://vijayantagupta.com/writing/the-second-growth-curve

- May 2026 SaaS Rebound public-market deck. https://docs.google.com/presentation/d/e/2PACX-1vStSy9dyXd43qu6o81eg_IBoVcpSLVRpFBA96f2Hnq4_jAm9IqJ3WQDqv-yKqmZ8P7GC1AkdmXMt4br/pub?start=false&pli=1

- FinancialContent. The 2026 SaaSpocalypse: Why B2B Software Stocks Are Plunging 20 per cent. 24 March 2026. https://markets.financialcontent.com/stocks/article/marketminute-2026-3-24-the-2026-saaspocalypse-why-b2b-software-stocks-are-plunging-20

- Humai. SaaSpocalypse: Why Enterprise Software Has Lost More Than 2 Trillion in 2026. 2026. https://www.humai.blog/saaspocalypse-why-enterprise-software-has-lost-more-than-2-trillion-in-2026/

- Fortune. The 3 forces quietly dismantling the business model that made enterprise software fabulously profitable. 17 April 2026. https://fortune.com/2026/04/17/ai-saas-enterprise-software-moats-margins-saaspocalypse/

- SaaSMag. The AI COGS Problem: SaaS Gross Margin Compression 2026. https://www.saasmag.com/ai-cogs-saas-gross-margin-compression/

- The SaaS Academy. How AI Changes SaaS Gross Margin: CFO Guide to AI COGS. 2026. https://www.thesaasacademy.com/blog/how-ai-changes-saas-pnl-gross-margin

- TechTimes. AI Agent Economics: Token Tax Locks Gross Margins 30 Points Below SaaS Baseline. 1 June 2026. https://www.techtimes.com/articles/317542/20260601/ai-agent-economics-token-tax-locks-gross-margins-30-points-below-saas-baseline.htm

- Bloomberg. Thoma Bravo, Vista Seek to Calm Fears Over AI Threat to Software. 11 February 2026. https://www.bloomberg.com/news/articles/2026-02-11/thoma-bravo-vista-seek-to-calm-fears-over-ai-threat-to-software

- Thoma Bravo. Completes Acquisition of PROS Holdings, Inc. https://www.thomabravo.com/press-releases/thoma-bravo-completes-acquisition-of-pros-holdings-inc

- NVIDIA Perspectives. CFOs: Shift to Token Economics for AI Cost Forecasting on NVIDIA Blackwell. 2026. https://perspectives.nvidia.com/cfo-budget-framework-ai-inference-cost-forecasting/